As global concerns for corporate sustainability continue to gain momentum, regulatory frameworks are evolving to ensure businesses align with environmental, social and governance (ESG) principles. One such development is the Corporate Sustainability Reporting Directive (CSRD), set to impact companies across Europe.

The CSRD creates a new era of transparency and accountability, introducing enhanced reporting requirements on sustainability matters for large EU companies (MNEs), listed SMEs and non-EU companies with significant activities in the EU. Besides the direct consequences for companies directly in scope, the CSRD will also indirectly impact SMEs through requests for sustainability information from business partners that need to comply and will have to report on their value chain, as mandated by CSRD. Other stakeholders that might request information from SMEs include banks, employees and customers.

To answer this growing pressure from stakeholders, even SMEs that are not under scope of the legislation can choose to publish a voluntary ESG reporting. By doing this, they can build trust with their stakeholders and show accountability, while also gaining direct economic benefits. Concrete examples are more beneficial interest rates when applying for loans at a bank, being able to apply for (public) grants and winning tenders with customers who are looking for sustainable suppliers.

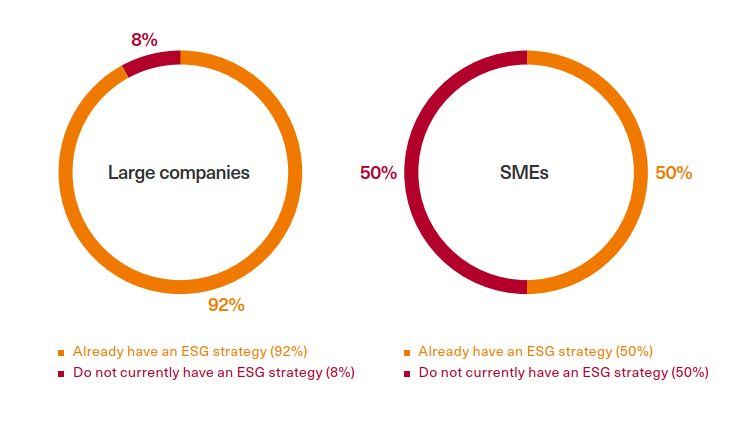

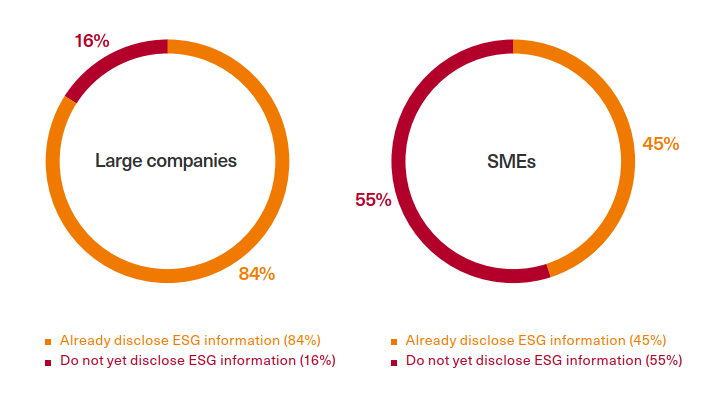

However, while larger corporations may have the resources to adapt swiftly, SMEs often face unique challenges when tackling ESG reporting.

The CSRD creates a new era of transparency and accountability, introducing enhanced reporting requirements on sustainability matters for large EU companies (MNEs), listed SMEs and non-EU companies with significant activities in the EU. Besides the direct consequences for companies directly in scope, the CSRD will also indirectly impact SMEs through requests for sustainability information from business partners that need to comply and will have to report on their value chain, as mandated by CSRD. Other stakeholders that might request information from SMEs include banks, employees and customers.

To answer this growing pressure from stakeholders, even SMEs that are not under scope of the legislation can choose to publish a voluntary ESG reporting. By doing this, they can build trust with their stakeholders and show accountability, while also gaining direct economic benefits. Concrete examples are more beneficial interest rates when applying for loans at a bank, being able to apply for (public) grants and winning tenders with customers who are looking for sustainable suppliers.

However, while larger corporations may have the resources to adapt swiftly, SMEs often face unique challenges when tackling ESG reporting.